What Investor Behavior Tells Us About Private Markets

Private markets have undergone a quiet but profound transformation over the past decade. Once viewed primarily as the domain of large institutions, they are increasingly becoming a central component of sophisticated individual portfolios. Recent investor research by Goldman Sachs offers valuable insight into how perceptions, allocations, and priorities are evolving, and what these shifts signal for long-term investors and business builders.

While market commentary often focuses on short-term sentiment, investor allocation behavior offers a more durable signal. The 2025 survey reveals not only continued interest in alternative investments but also a maturing perspective on risk, liquidity, and long-term value creation.

For TZG, these findings echo themes we observe across private market transactions, investor dialogue, and capital formation dynamics.

Alternatives Adoption Reflects Portfolio Maturity

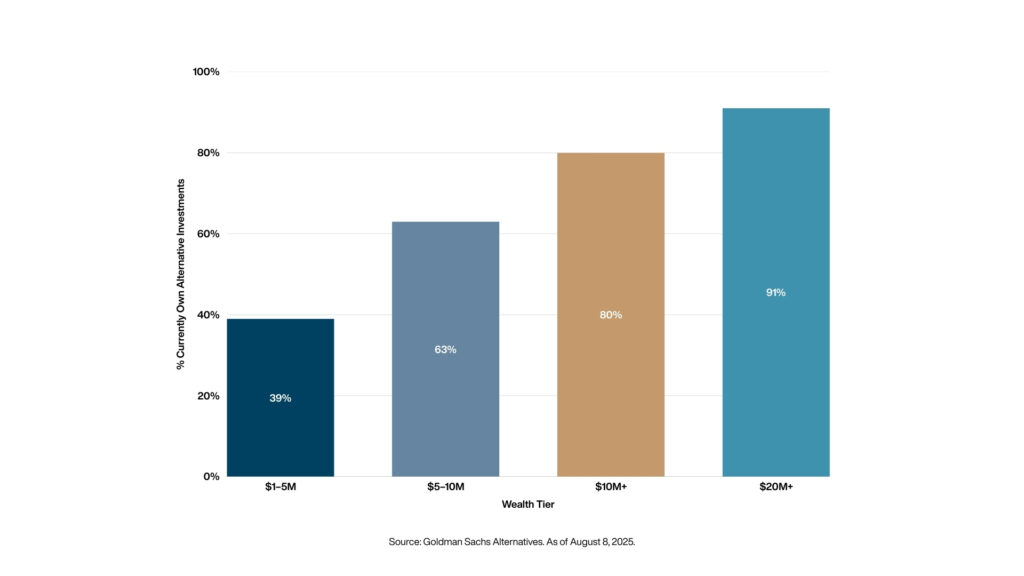

One of the most consistent patterns emerging from investor data is the relationship between wealth and alternatives adoption. As portfolios grow, allocations to private equity, private credit, and private real estate tend to increase meaningfully.

Investors in the lower wealth tiers often prioritize liquidity and capital preservation. However, beyond certain portfolio thresholds, alternatives adoption accelerates sharply. This inflection point suggests that exposure to private markets increasingly becomes not an opportunistic choice, but a structural allocation decision.

For experienced investors, alternatives serve several strategic purposes:

- Traditional equity/bond portfolios face structural challenges

- Return dispersion is widening

- Diversification benefits of private markets remain compelling

- Reduced reliance on public market cycles

Risk Perception vs. Investment Reality

Despite growing adoption, a significant number of investors continue to label alternative investments as “high risk.” This perception often stems from concerns about illiquidity, complexity, or unfamiliarity rather than underlying asset fundamentals.

Interestingly, research shows a notable divergence between perception and experience. Investors already allocating to alternatives frequently rate them as less risky than non-users. Familiarity, transparency, and time horizon alignment appear to reshape risk interpretation.

Illiquidity, in particular, remains widely misunderstood. For investors with long-term capital and disciplined portfolio construction, reduced liquidity is not inherently a disadvantage. In many cases, it serves as a structural feature that supports long-duration value creation strategies.

Growth Increasingly Resides in Private Markets

Another structural factor driving investor behavior is the changing composition of the global business landscape. The number of publicly listed companies has declined significantly over recent decades, while private equity-backed enterprises have multiplied.

Many of today’s most dynamic companies choose to remain private longer. They seek operational flexibility, long-term capital alignment, and reduced short-term market pressures. As a result, a growing share of innovation, transformation, and value creation occurs outside public exchanges.

For investors focused on capturing these growth dynamics, private markets are evolving from “alternative” to “essential.”

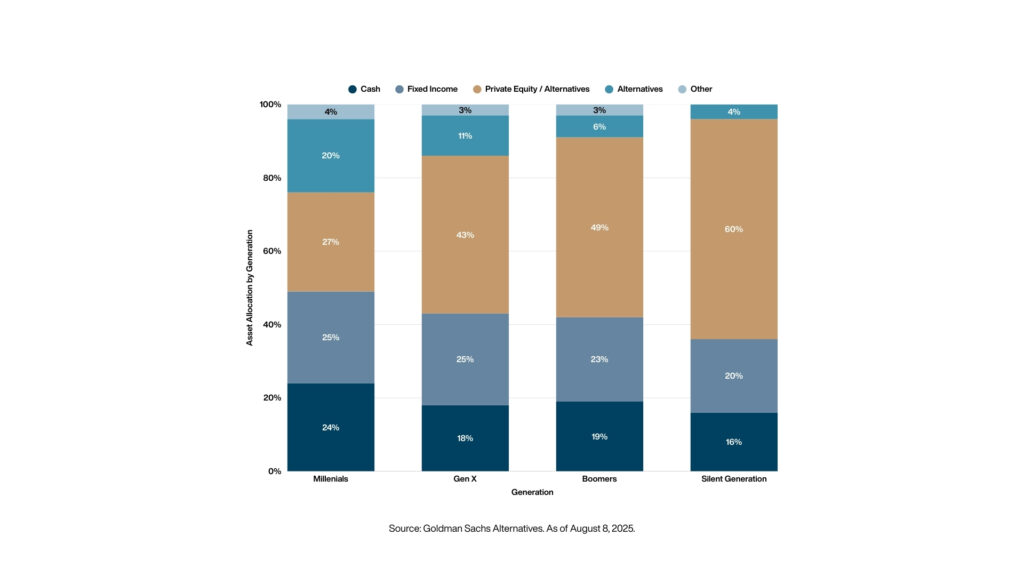

The Generational Reframing of Portfolio Strategy

Generational differences further reinforce this trajectory. Younger investors demonstrate higher familiarity with alternatives and greater openness to private market exposure. Their motivations often extend beyond diversification toward:

- Access to innovation

- Unique investment opportunities

- Long-term capital growth

- Differentiated sources of return

This shift reflects not only changing product accessibility but also a broader reframing of portfolio construction philosophy.

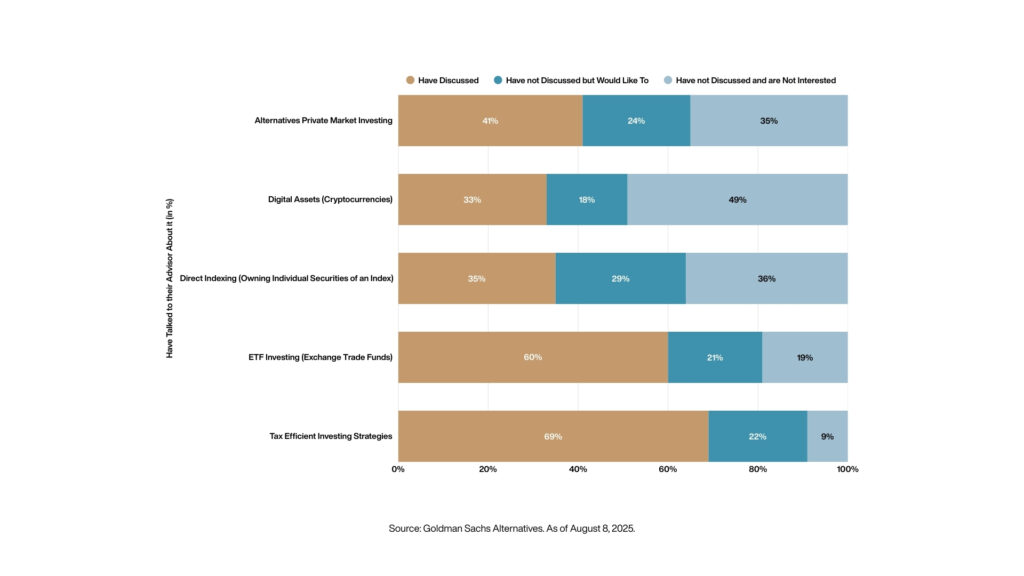

Education and Clarity Remain Critical

While adoption trends are clear, research also highlights a persistent education gap. Alternatives are discussed less frequently between advisors and clients compared to traditional products such as ETFs or tax strategies.

As private markets continue to expand their role, investor outcomes will increasingly depend on:

- Clarity of objectives

- Understanding of liquidity profiles

- Alignment with time horizons

- Selection of experienced partners

- Thoughtful portfolio integration

The TZG Perspective

Investor behavior offers more than a snapshot of allocation preferences. It reflects a deeper recognition that markets, businesses, and value creation pathways are evolving.

For long-term investors, the conversation is shifting from “Should alternatives be included?” to “How should alternatives be integrated intelligently?”

For operators and business builders, this shift reinforces the enduring relevance of private ownership structures that prioritize patience, discipline, and long-term strategy execution.

We have long believed that durable value is built through disciplined execution, strong partnerships, and patient capital. Private markets naturally align with these principles. They provide an environment where transformation, operational excellence, and long-term thinking can compound over time.

As investor behavior continues to evolve, it becomes increasingly evident that private markets are not simply expanding, they are redefining the architecture of investing. They continue to offer compelling opportunities for disciplined investors focused on operational effectiveness, resilience, and long-term value creation.

See the full original research document here

We welcome thoughtful conversations and exchange of ideas with founders, operators, and investors.